Service Models

Service Models Market Access

Market Access Institutional Custody

Institutional Custody Tax and Compliance

Tax and Compliance Research and Data

Research and Data  Asset Managers and ETPs

Asset Managers and ETPs Banks and Fintechs

Banks and Fintechs Specialty Lenders

Specialty Lenders  Asset Segregation

Asset Segregation Custody Protocol

Custody Protocol Proof‑of‑Reserves

Proof‑of‑Reserves Insurance Coverage

Insurance Coverage Authorizations

Authorizations SOC Attestations

SOC Attestations AML

AML Regulations

Regulations  About CheckSig Clear

About CheckSig Clear FAQ

FAQ News and Insights

News and InsightsBitcoin: 2026 opens with a correction, but fundamentals remain strong

April 16, 2026 - Staff

The first quarter of 2026 confirms a corrective phase across the crypto ecosystem. Price retracement, declining volatility, and low correlation with traditional asset classes point to a compelling opportunity for investment and portfolio diversification.

Milan, April 16, 2026 – The Digital Gold Institute, the research division of CheckSig and Europe’s leading think tank focused on Bitcoin, crypto-assets, and blockchain, has published the 29th edition of its quarterly report on the crypto ecosystem.

Bitcoin under pressure

Bitcoin closed Q1 down 24%, marking its second consecutive negative quarter.

This correction does not undermine the sector’s fundamentals, which remain solid. Market activity and liquidity continue at elevated levels, with trading volumes close to historical highs. ETF and derivatives exposure also remains strong, confirming sustained and widespread investor interest. The current phase appears to be driven more by profit-taking and capital reallocation than by any structural contraction of the sector.

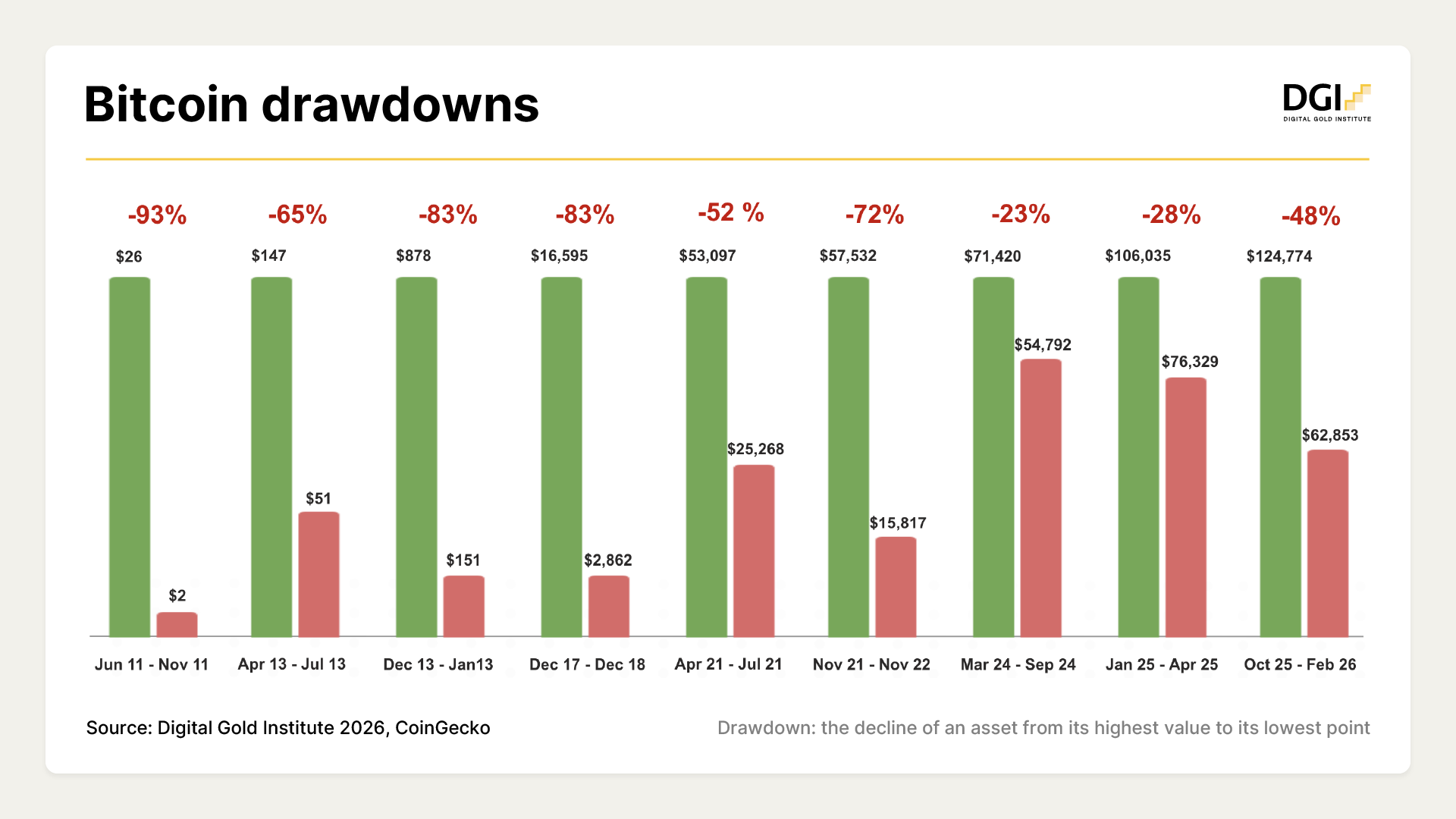

Limited drawdowns: a sign of market maturity

In this context, the evolution of Bitcoin drawdowns—declines from previous all-time highs—is particularly noteworthy. Downside movements are becoming less severe compared to past cycles, indicating a strengthening market structure and a growing presence of long-term investors.

Bitcoin remains central to portfolio construction

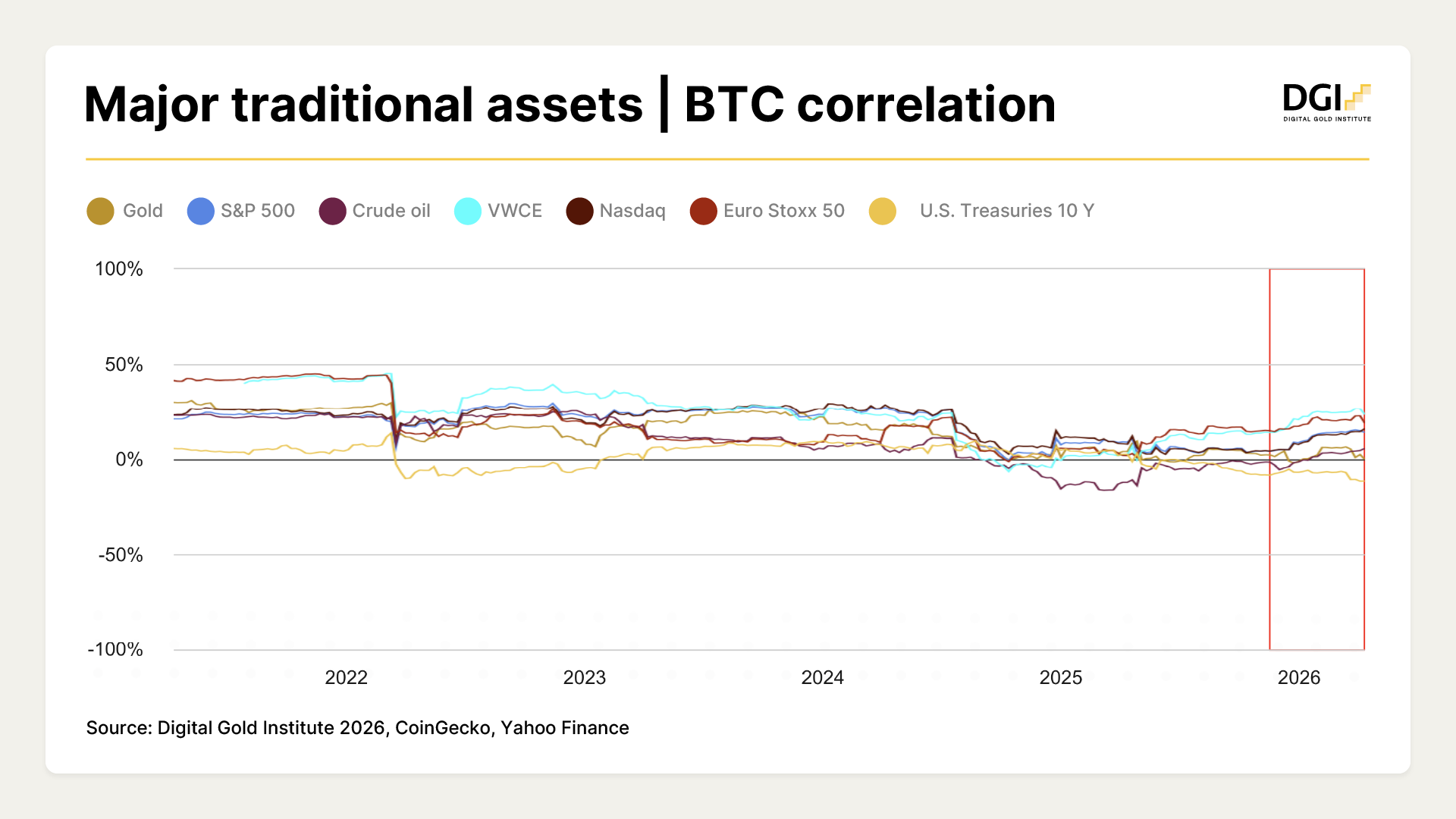

From a portfolio construction perspective, the quarter has not altered correlation dynamics. Bitcoin’s low correlation with traditional asset classes reinforces its role as an effective diversification tool within multi-asset portfolios.

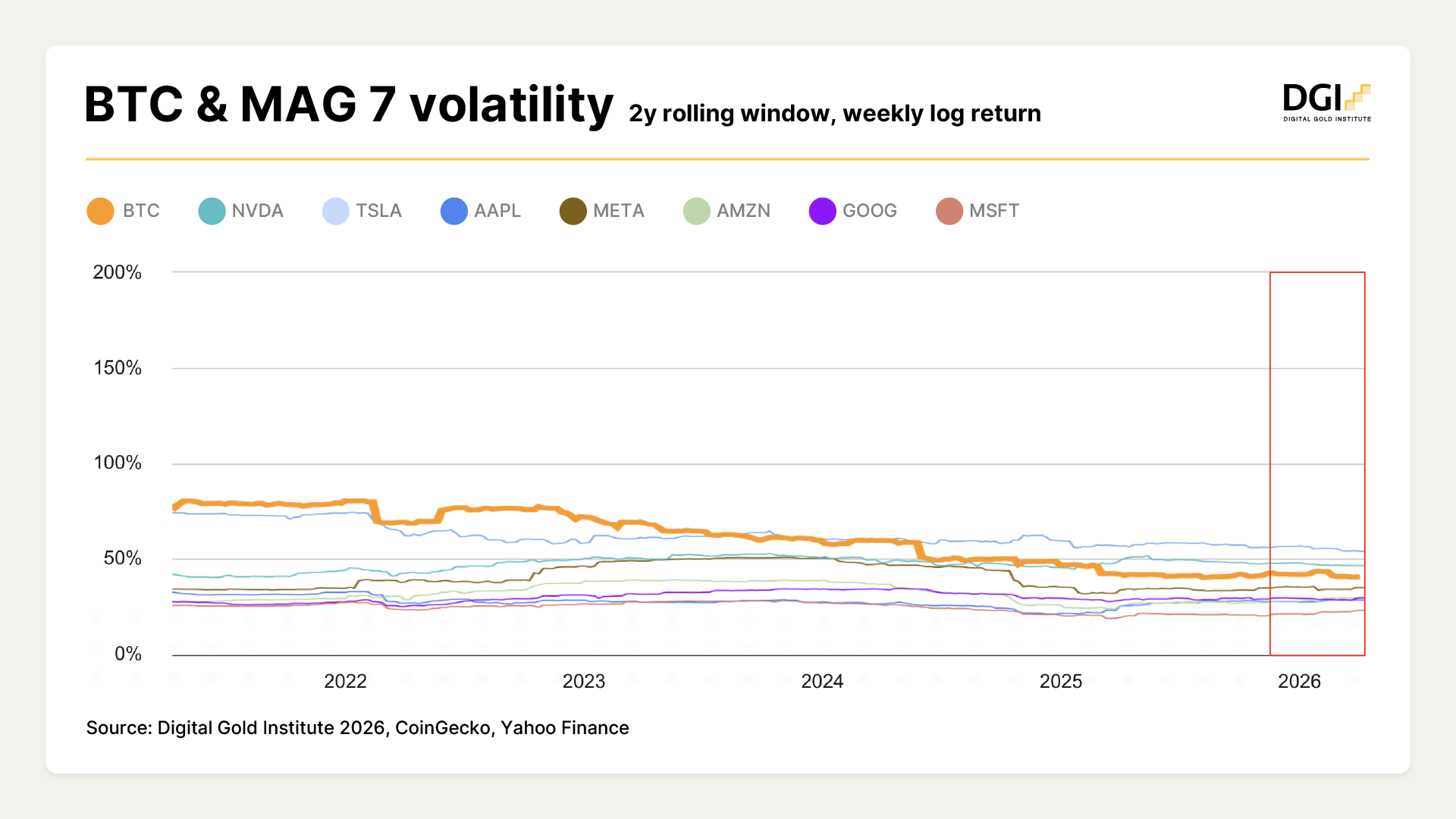

Bitcoin continues to stand out as a strategic investment, capable of enhancing risk-adjusted returns while maintaining significant growth potential. Its volatility profile is now broadly in line with that of the so-called “Magnificent 7” equities.

According to Ferdinando Ametrano, CEO of CheckSig, ”the current price retracement, combined with declining volatility and low correlation, represents a remarkable opportunity for investors seeking diversification and allocation efficiency.”

Altcoins struggle and offer limited diversification benefits

The first quarter of 2026 confirmed a broad market correction across crypto-assets alongside Bitcoin. However, Bitcoin has demonstrated greater resilience than major altcoins, which recorded sharper losses: Ether fell by 32%, Solana by 34%, and Ripple by 29%.

Bitcoin continues to dominate the crypto market, accounting for 60% of total market capitalization. Moreover, major crypto-assets continue to move largely in tandem with Bitcoin, confirming limited diversification benefits within the asset class itself.

European regulation: MiCA licenses rise, Italy lags behind

On the regulatory front, as of March 31, 2026, a total of 182 MiCA licenses have been granted, with a strong concentration in key European countries. Germany, the Netherlands, and France account for approximately 50% of the total, highlighting the sector’s progressive integration into the regulated financial framework.

Italy, however, remains behind, standing as the only major European economy yet to begin issuing licenses. In this context, recent leadership changes at CONSOB could mark the beginning of a new phase for a sector that has so far been hindered by a restrictive regulatory approach.

Bitcoin and gold: complementary inflation hedges

The session concluded with a keynote by Daniele Bernardi, CEO of Diaman Partners, focusing on gold and Bitcoin as potential hedges against rising inflation.

According to Bernardi, in an inflationary scenario, choosing between gold and Bitcoin is the wrong question to ask. Gold hedges equity risk, while Bitcoin hedges bond risk. Together—within an allocation that dynamically adapts to market conditions—they become something more: a capital protection framework that traditional portfolios do not provide.

The next Digital Gold Institute report is scheduled for July 2026.